यह भी देखें

15.05.2026 12:41 AM

15.05.2026 12:41 AM

Currently, the topic of US inflation and its consequences is actively discussed in the currency market. Due to geopolitical factors, inflation has not taken center stage, although its effects are evident to many. There is little positivity within those effects. However, the market is not in a hurry to draw conclusions, as there are too many variables and unknowns in the current equation. Let's try to unpack this.

Before the geopolitical conflict in the Middle East and during Donald Trump's presidency, the scenario would be quite straightforward. If inflation rises, the central bank should raise interest rates. An increase in the interest rate is a plus for the US currency. However, for the past year and a half, the Federal Reserve's monetary policy has been overshadowed by Trump's policies. If the US dollar is not plummeting like a rock to the Mariana Trench, it is consistently leaning towards decline. Even the supposed shift of the Fed to a "hawkish" stance does not change this.

Moreover, Trump continues to demand a softening of the policy. This is why he sought to oust "hawks" within the FOMC, including Jerome Powell himself. As everyone knows, Powell remains on the committee, and Kevin Warsh has predictably become the new chair. However, what changes in Fed policy are likely if inflation is rising, making it practically impossible to lower interest rates?

This is where things get interesting. Warsh and Stephen Miran will find grounds for policy easing. They do not have to look far—the American economy is slowing, and the labor market needs support. However, it is highly likely that Warsh and Miran will remain in the minority during FOMC votes, while Powell will keep a close watch over Fed officials, preventing them from even considering siding with Trump.

Thus, a rate cut seems practically impossible under the current circumstances, while raising rates would further hurt the US economy and labor market. Nevertheless, Trump will continue demanding lower rates, while inflation will keep accelerating. What does all this mean? In my view, the most straightforward scenario. The dollar will not change its course due to this "soap opera." The market priced in Trump's trade war last year, and in 2026, it is primarily concerned with Middle Eastern geopolitics. It is very likely that the Fed will not change the rate even once this year, and behind-the-scenes intrigues will interest few—there are more pressing topics in the market right now.

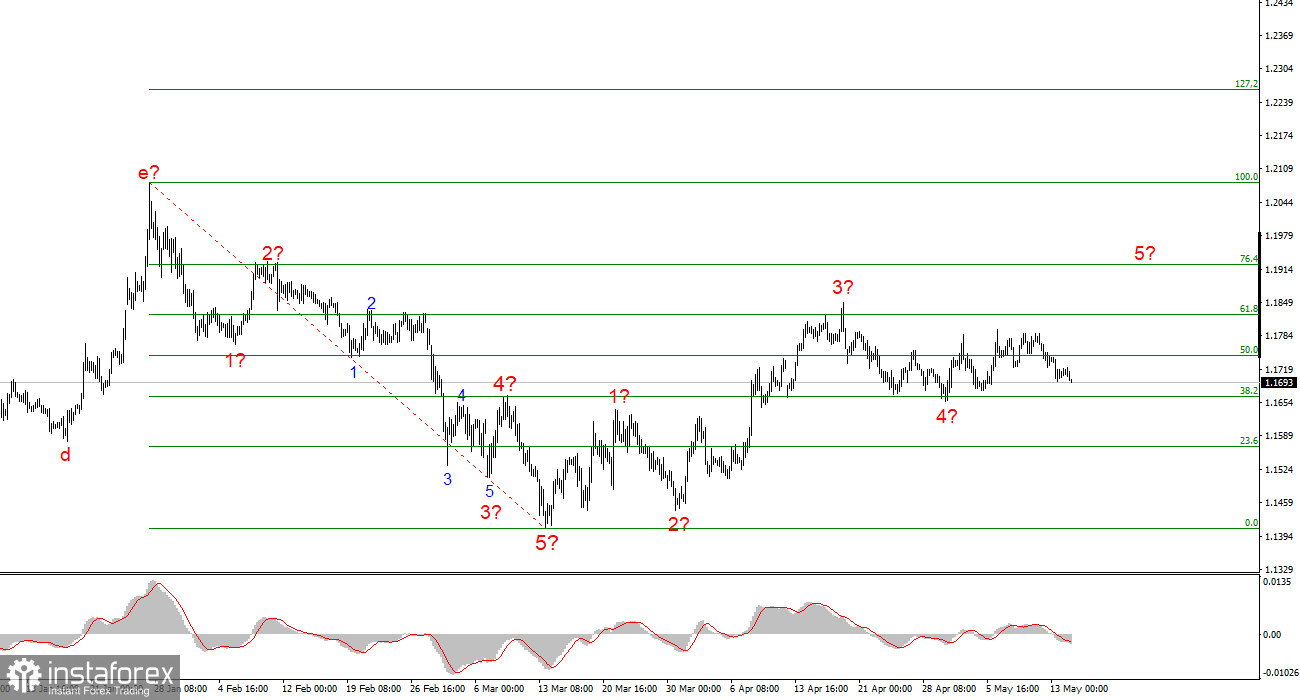

Based on the analysis of EUR/USD, I conclude that the instrument remains within the upward segment of the trend (see the lower chart), while in the short term, it is within a corrective structure. The corrective wave setup appears quite complete and may evolve into a more complex, elongated form. However, for that to happen, the geopolitical backdrop in the Middle East needs to improve, rather than worsen. Therefore, without positive news, I expect the instrument to decline below the 1.1665 mark, which corresponds to 38.2% on the Fibonacci scale.

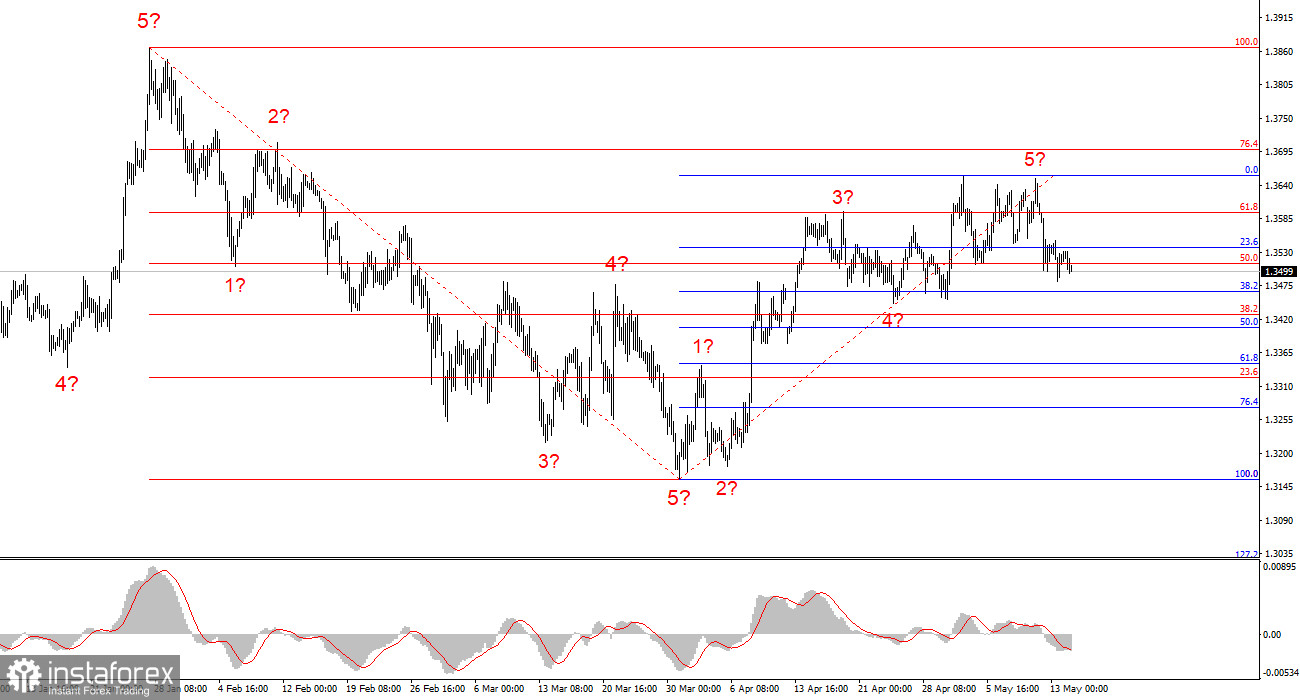

The wave structure of the GBP/USD instrument has become clearer over time, as I anticipated. We now see a clear five-wave upward structure on the charts, which may be completed soon. If this is indeed the case, we can expect a corrective wave setup to form after wave 5 completes. Wave 5 may be completed around the 1.3699 mark, which corresponds to 76.4% on the Fibonacci scale. If geopolitics continues to move toward long-term peace, a new bullish segment of the trend may begin after the correction wave setup concludes. Therefore, the combination of waves and geopolitical factors will determine the pound's fate in the coming weeks.