Veja também

27.01.2026 02:57 PM

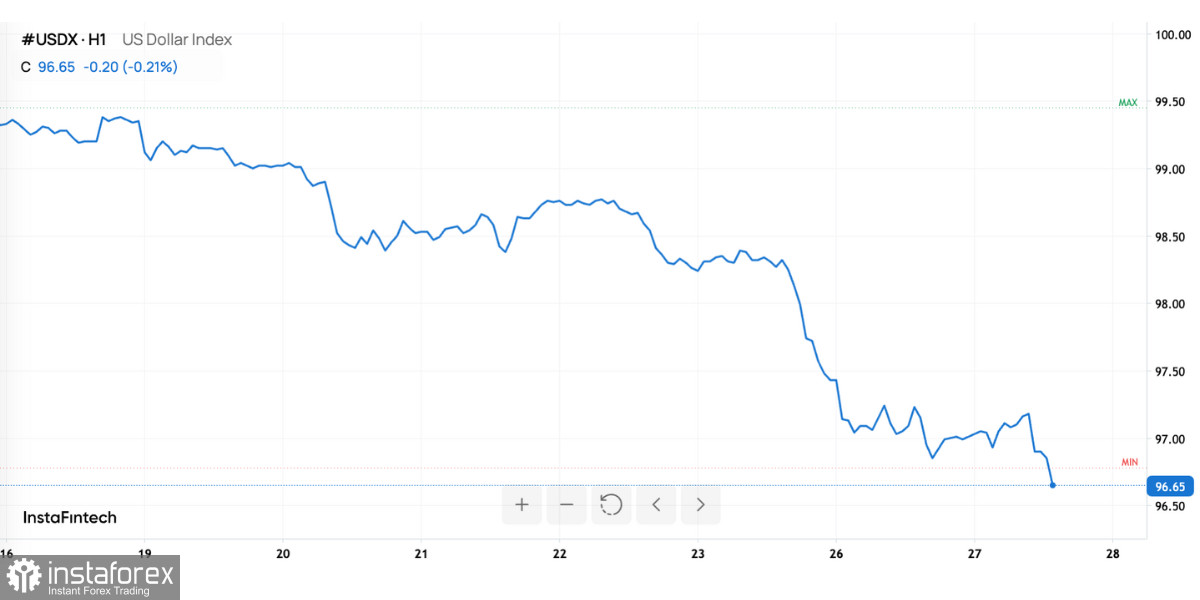

27.01.2026 02:57 PMAhead of the Federal Reserve's two?day meeting on January 27–28, the dollar arrives in a state that is simultaneously calm and potentially unstable for markets. The formal interest rate decision is barely in dispute: consensus expects the policy rate to be left in the 3.50–3.75% range. That means the mere fact of the decision is already priced in and is unlikely to be a new impulse for the dollar. However, such moments are often the most sensitive — when the market stops reacting to "what" and begins to react sharply to "how" and "why."

In the current configuration, the dollar is not trading as a reflection of the current policy rate but as an expression of expectations about future monetary policy. For market participants, the key question is not what the Fed will do now but how durable and long?lasting the regulator considers the regime of tight financial conditions to be. Any signals about the anticipated length of that regime directly affect expectations for yields on dollar assets and, therefore, demand for the dollar itself.

When the market is convinced that rates will stay higher for longer, the US dollar is supported through several channels. First, dollar instruments become relatively more attractive versus alternatives. Second, the dollar's role as a funding currency and liquidity reservoir strengthens. Third, investors become less willing to position for dollar weakness, since the risk of premature easing appears limited.

At the same time, it is important to understand that when the base scenario is already "set," the dollar becomes especially sensitive to rhetorical nuances. The market will watch the Fed's wording closely — the balance between mentions of inflationary and economic risks and any signals about how comfortable the regulator feels with current conditions. Even small shifts in emphasis can trigger a reshaping of expectations and moves in the greenback, not because facts changed but because their interpretation did.

Macro data, debt market, and institutional risk factor

Before the Fed announces its decision, the dollar must pass several interim tests, each of which can strengthen or weaken current expectations. Publication of consumer confidence data acts as a quick barometer of domestic demand. For FX markets, this matters not by itself but through its impact on perceptions of economic resilience. A more confident consumer is an argument that the economy can withstand tight conditions, and therefore the Fed will not need to rush to ease — a logic that supports the dollar via rate expectations.

Even moderate misses or beats in the confidence index ahead of the Fed meeting can produce a noticeable dollar reaction. On such days, the market becomes less tolerant of uncertainty and quicker to respond to signals that could shift the balance of arguments within the Fed.

An equally important factor for intraday trading is the $70bn auction of 5?year Treasury notes. For the dollar, this is a key point of contact with the debt market. Demand for the auction — or lack thereof — is directly reflected in medium?segment yields, which are particularly sensitive to expectations about future Fed policy. Strong demand signals investors' willingness to hold dollar duration at current yield levels, whereas weak placement could increase pressure on yields and alter the near?term USD profile.

Overlaying these factors is the political?institutional backdrop around the Fed. Heightened attention to legal and personnel questions increases uncertainty and raises the risk premium. This has a dual effect on the dollar. On one hand, rising uncertainty often supports demand for liquidity, and the dollar remains the primary liquidity vehicle. On the other hand, the market's sensitivity to the regulator's communication increases: any wording is read through the prism of institutional resilience and policy predictability.

As a result, the dollar is in a heightened state of susceptibility. It is not expecting a rate surprise, but it is extremely sensitive to how the Fed frames the narrative about the economy and its intentions. That narrative will determine whether the US dollar stays supported by expectations of high interest rates for an extended period or faces a need to reprice positions.

In essence, the current moment for the dollar is a trust test — trust that tight policy rests on solid foundations and trust that the Fed controls the trajectory it is following. The market will try to extract the answer not from the rate number, but from the Fed's words and tone.